For the first time in history, the annual Jackson Hole economic meeting was a virtual affair this year thanks to Coronavirus. Jerome Powell, Federal Reserve Chairman took this opportunity to set out an important but low-key shift in Fed policy. The new policy framework heralds a clear departure from central bank thinking of the past several years. We discuss the implications of this change and our views in this update.

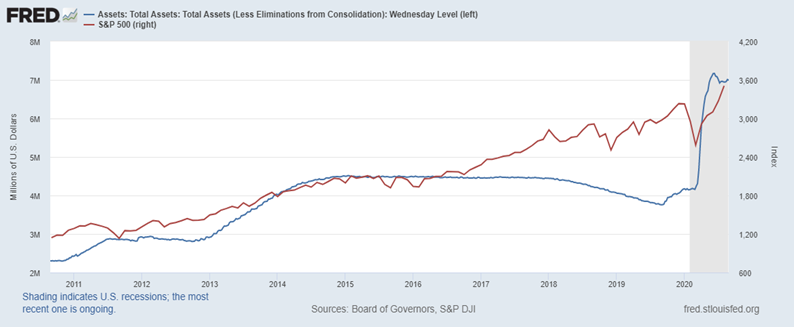

Since our last update, the S&P 500 has successfully pushed onto a new high above 3500 as anticipated. On the other hand, US Treasury yields have moved upwards at the medium to longer end, with the 10-year now yielding a shade over 0.70%, a little sooner than we expected. The unprecedented monetary and fiscal policy response to COVID-19 has prevented a banking crisis. These extraordinary measures have also fuelled a meteoric rise in equity indices, divorced from the economic fundamentals. Technology has been a major beneficiary. Investor portfolios have largely recovered although the economics must rapidly play catch-up to avoid a relapse. The following chart visualises the magnitude and support central banks have provided to risk assets so far.

For the best part of the last two quarters, central banks and governments alike have focused on keeping their economies on ventilators (this ventilator is estimated to cost over $10tr once the COVID-19 episode is over). Inevitably, the result is excess liquidity and higher asset prices, as well as encouragement of leveraging with an implicit “Fed guarantee” applied to mainstream asset prices. Overarching central bank policy has also impeded the ability of efficient capital markets to allocate capital to deserving business models, by rescuing the worthy and the unworthy alike.

At the Jackson Hole meeting last week, the Fed Chairman updated the “Longer-Term Goals on Monetary Policy” and signalled the Fed will change its method of inflation targeting and, in the future, will target average inflation of 2%. Previously, the Fed had simply targeted core inflation of 2%. One of the reasons for this change in policy can be traced to the magnitude of money injected into the economy via quantitative easing.

This excess liquidity is fuelling, and will further fuel, asset prices and inflation above 2% over the longer term, hence the use of an “averaging mechanism”. As we have previously stated, the fall in the value of the US dollar is another direct consequence, albeit a positive one, of a broader economic recovery amongst dollar dependent economies.

The likely resurgence of inflation could impact the price stability of Treasuries and by extension, all debt, except if the Fed keeps Treasury demand high by direct market action. This in turn will expand the Fed’s balance sheet beyond current levels and further extend Modern Monetary Theory. Recent data is starting to indicate the possibility of increased short-term pressure on equity prices.

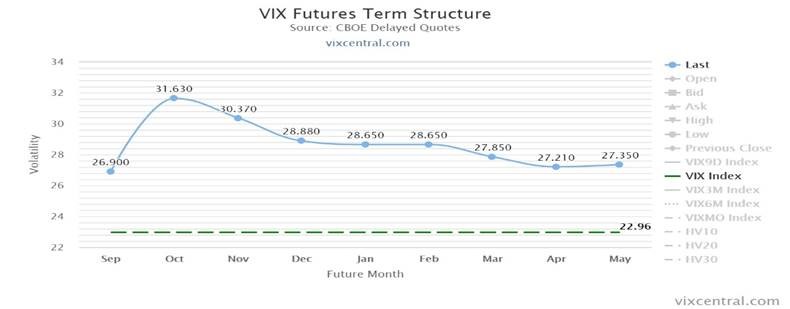

Valuations remain extremely high by long-term standards, recent market highs have been fuelled, surprisingly perhaps, by faltering momentum. As we had anticipated, a 3600 level in the S&P 500 Index is achievable, but a confluence of events and indicators signal a possible pullback in the short-term in the absence of a positive surprise or even more central bank activity. Volatility is expected to increase before the US elections set for November, as shown by the chart above.

Over the medium- to longer-term, risk assets remain well supported by a recovering global economy, historically low interest rates, and central government spending. We expect inflation to push risk asset prices further in the medium term. We also expect some investor capital to switch from fixed income to risk assets once vaccine delivery news becomes tangible.

Read more articles like this on our insights page

About the author

Asim Javed, CFA, Senior Investment Manager

Asim Javed is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years’ investment management and portfolio oversight experience.

This communication is from Alpha Beta Partners Limited an Appointed Representative of Oakham Wealth Management Limited, Registered in England at Berkeley Square House, Berkeley Square, London, England, W1J 6BD. Oakham Wealth Limited is authorised and regulated by the Financial Conduct Authority. Reference No. 431206 . Alpha Beta Partners Limited – reference number 799887.The information in this email, and those ensuing, is confidential and may be legally privileged. It is intended solely for the addressee. If you are not the intended recipient(s) please note that any form of disclosure, distribution, copying or use of this communication or the information in it or in any attachments is strictly prohibited and may be unlawful. If you have received this communication in error please destroy this message and any copies of it and kindly notify us immediately-mail communications may not be secure and may contain errors. Where possible, confidential data should be sent to us in encrypted form. This e-mail will have been scanned by our anti-virus software before transmission. We cannot however, warrant that this e-mail is free from viruses. We do not accept liability for the consequences of any viruses that may be inadvertently be attached to this e-mail. Anyone who communicates with us by e-mail is taken to accept the risks in doing so. When addressed to our clients, any opinions or advice contained in this e-mail and any attachments are subject to the terms of business in force between Alpha Beta Partners Limited and the client. Alpha Beta Partners Ltd. 4 Lombard Street, London EC3V 9AA [email protected] I 020 8059 0250

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Asim Javed, Alpha Beta Partners

Asim is a highly qualified Senior Investment Manager and Risk Manager. He is a Chartered Financial Analyst (CFA) charter holder and a Chartered Accountant with over ten years investment management and portfolio oversight experience.

Read more articles by this author

Be the first to hear news and insights from Embark Pensions

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.