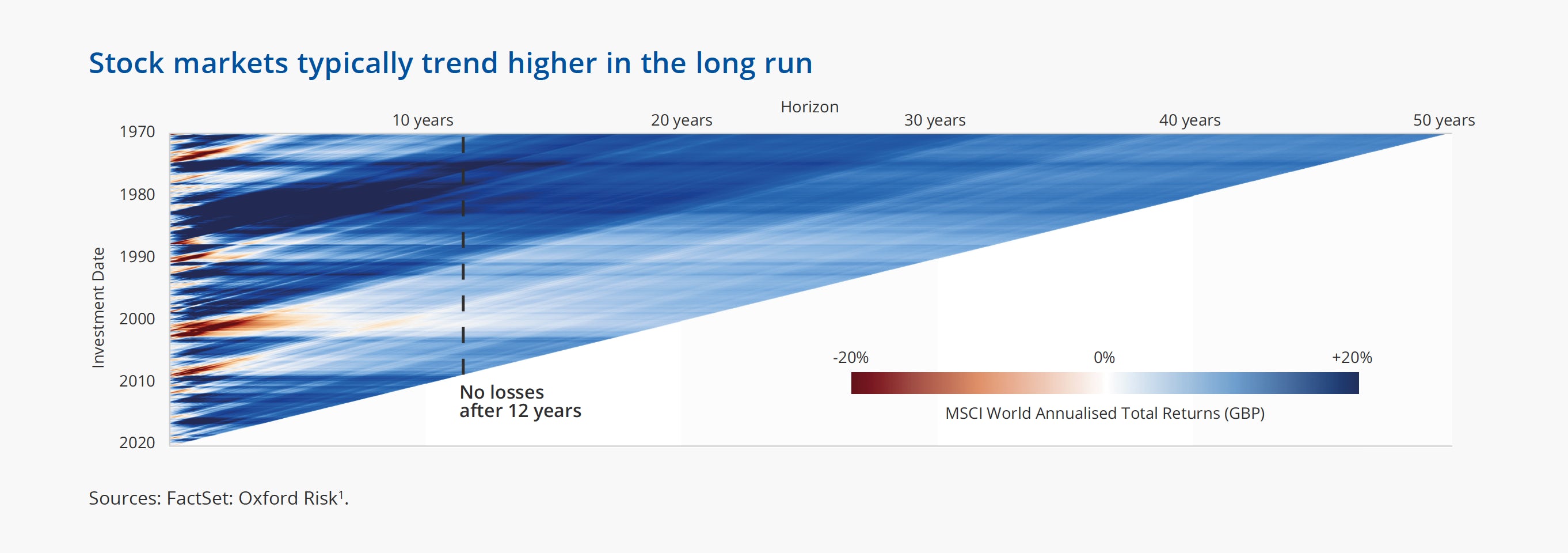

Stock markets have performed poorly so far in 2022, particularly US stock markets like the S&P500 and the Nasdaq Composite which delivered double-digit percentage declines to the end of the June. This does, however, come after some historically strong positive returns in the preceding years. Stock markets typically produce positive returns in the longer-term – the chart shows all investments since 1970 in the MSCI World Index retained for over 12 years have produced positive returns.

Market corrections are an inevitable feature of investing as economic conditions wax and wane from good to bad and back again, but they can be difficult times to navigate for investors. This is because investing is prone to being derailed by a range of common psychological biases that can trigger emotional decision-making. And emotionally made decisions can be hazardous to building long-term portfolio wealth. This article looks at some of the major psychological traps that investors can fall into and how advisers can help their clients to avoid them.

Don’t overtrade or change strategies – it’s bad for long-term returns

If ‘time in the market beats timing the market’ is a well-worn expression in investing circles, it is with good reason – it is one investing proverb that is totally borne out by the data. By analysing the transaction data of over 60,000 investors in a brokerage company during the 1990s, Barber and Odean (2000) found that the average after-cost return for investors who traded the most was 11.4%, which compared to 18.5% for those who traded the least, while the market return was 17.9%.*

A material driver of the underperformance was the increased transaction costs associated with higher portfolio turnover, but overconfidence was also a factor. For those more active investors who take a keen interest in their portfolios and who also believe they can time market cycles, the evidence is far from compelling.

“The investor’s chief problem—and even his worst enemy—is likely to be himself.”

Benjamin Graham

Investor takeaway: Decide on a long-term investment strategy with your adviser that is appropriate to your risk appetite and capacity for loss and then just stay the course. The evidence suggests chopping and changing is often a path to lower returns.

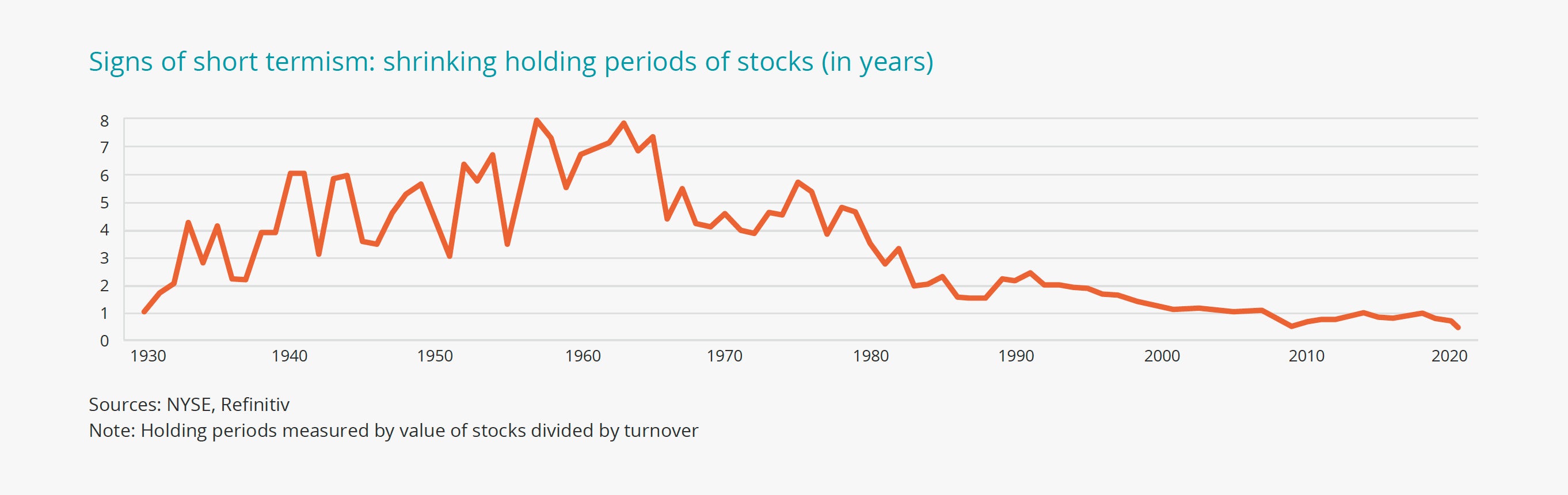

The problem of short termism in markets has been steadily getting worse. Evidence from major stock exchanges highlights that investors have become more short-term over time. In the US, the average holding period of a share on the NYSE was around seven years in the 1960s; by June 2020 this had fallen to only six months. Short termism is not something that is confined to end investors either – even the focus of Wall Street analysts is overwhelmingly on forecasting company earnings for only the next one or two years.

“When an investor focuses on short-term investments, he or she is observing the variability of the portfolio, not the returns – in short, being fooled by randomness.”

Nassim Nicholas Taleb

Investor takeaway: The best way to get an edge in an increasingly myopic market, dominated by high frequency traders like hedge funds and day traders, is to take a longer-term view than the market.

Don’t blindly follow the herd

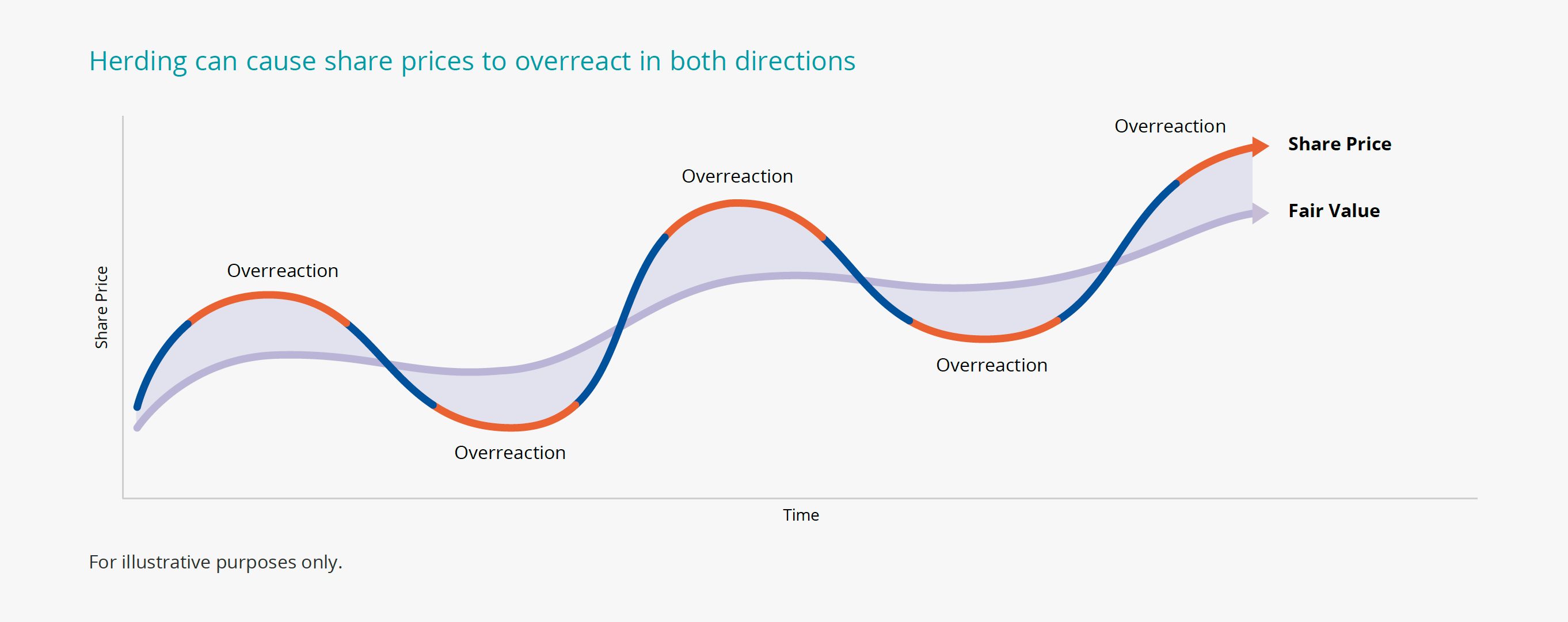

Given the strong herding instinct in asset markets, a bout of selling pressure can prompt some investors to question their own investment choices. Why are other investors selling? Do they know something I don’t? Should I be selling too? The evidence suggests the answers to these questions can be surprisingly irrational. In his analysis of the 1987 stock market crash, Robert Shiller demonstrated that when investors were asked why they were selling, many said ‘because everyone else was selling’.◊

In stock markets, groupthink and herd-like reactions can cause share prices to move away from fair values and overreact in both directions. Share prices can get a little ahead of themselves when everyone is wildly optimistic and subsequently get oversold when everybody becomes much too gloomy. For longer-term investors in risk-aligned multi-asset funds, such times are a reminder that it is the outcome not the path that is critical in the patient accumulation phase of building a pension pot.

Investor takeaway: Don’t fall into the trap of copying other investors’ moves, they may have completely different strategies with shorter time horizons, or they may be forced or distressed sellers.

Avoid buyer’s remorse

History shows that different assets perform well at different times. However, there is a psychological pain known as buyer’s remorse attached to investing in a chosen asset that subsequently performs poorly. Regret is one of the strongest felt human emotions and it is typically more pronounced the narrower and riskier the investment strategy. Buyer’s remorse tends to be very high (and painful) for those investors with their entire portfolio allocated to a single asset class or equity sector fund when that asset or sector subsequently underperforms.

“More money has been lost trying to anticipate and protect from corrections than actually in them.”

Peter Lynch

Investor takeaway: Multi asset funds can offer a simple but effective way of dealing with ‘buyer’s remorse’. By investing in a range of assets with different risk and reward characteristics, investors can avoid the binary pain associated with putting too much of their firepower in one asset only to see it fall out of favour.

Final thoughts

A long-term, risk-aligned investment strategy teamed with the discipline to stay the course can be a powerful combination in avoiding a wide range of potentially damaging emotional investing biases. The ability to focus on the long-term outcome and not become overly concerned about the path is a critical part of every patient investor’s journey. Volatile times are when that discipline is most tested.

For investors in risk-profiled multi asset funds, a large part of dealing with market volatility is considered at the outset thanks to a risk-defined, mixed exposure to growth and defensive assets. Moreover, advisers who can model the impact of correction events on their clients’ pension pots can put in vital groundwork to keep clients’ emotions in check.

Notes

^ Past performance is not necessarily a guide to future performance and the value of investments (and any income from them) can go down, so an investor may get back less than the amount invested.

* Brad Barber & Terence Odean; “Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors”, Journal of Finance, (April 2000)

˜ McClure, Laibson, Lowenstein & Cohen, “Separate neural systems value immediate and delayed monetary rewards” published in Science (October 2004).

◊ Robert J Shiller, ‘Investor Behavior in the October 1987 Stock Market Crash: Survey Evidence’

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on or treated as a substitute for specific advice of any kind.

We make no warranties, representations or undertakings about any of the content of this website; including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representations, warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Nick Armet, Content Strategy Lead, Embark Group

Nick Armet is Content Strategy Lead at Embark Group, responsible for creating, curating & managing content. Before joining Embark, Nick spent 10 years at Fidelity International where he was Head of Investment Communications, responsible for running a team that produced portfolio manager outlooks and non-product thought leadership on investment assets, markets and themes. Prior to that he was Head of Investment Writing at Standard Life Investments (now abdrn). Nick has an MA (Honours) Degree in Economics & Economic History from the University of Edinburgh.

Read more articles by this author

Be the first to hear news and insights from Embark Pensions

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.