Is it time for advisers to revisit the merits of fettered funds compared to their unfettered rivals?

The debate is not a new one, but given radical changes in regulation, market practices and approaches to advice and investing over the past decade or so, it is now framed in a dramatically different context.

Before we dive into it, a quick review of terminology. We consider fettered funds, like much of the industry, as a fund with a mandate to invest more than 80% in funds managed by the same investment company. Unfettered funds, on the other hand, are free to invest in funds run by other managers.

The nature of the debate has shifted from one that was primarily about performance to one that is now equally concerned with the control of risk, the maintenance of a clear investment strategy and the control of costs.

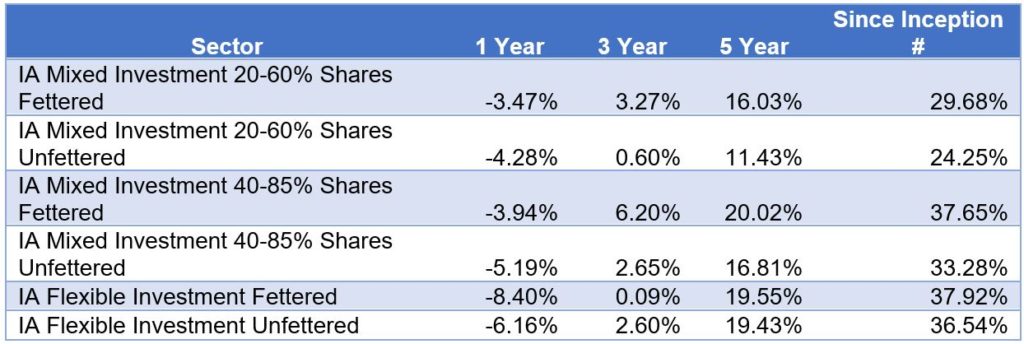

These broader criteria boost the case for a fettered approach—which we will explore in more detail later—however, there is a strong case based on performance as well. A comparison of fettered funds with their unfettered counterparts shows outperformance in the majority of scenarios since 2015. See below table:

(Source: FE fundinfo)

It’s also worth setting the historical context to understand how some of the established thinking has been arrived at.

The move to unfettered fund structures came about as part of the evolution of financial advice and financial services in general in the 90s and early 2000s. Over time the market moved from a choice of single providers of pensions, bonds and ISAs to one with significantly greater choice and more specialist fund management.

Some providers moved to offer a fettered choice of their own funds. Others created what became known as open architecture or unfettered funds. The latter were usually regarded as the better option of the two at the time, owing to their ability to access the whole range of asset classes.

However, although the advice profession, investment platforms and investment management have continued to evolve, the fettered and unfettered debate has got a little stuck in the past.

Selection

Picking a selection of well-regarded funds to provide diversification across a range of sectors was a significant improvement on the previous single provider approach, but it still risked managers doubling up on assets, sectors or geographies and even cancelling out overweight positions from one manager with underweight positions from another.

Although tools have become available to screen out some of that duplication risk and to improve diversification over the years, open selections still retain some of the old problems.

Moreover, more comprehensive and controlled fettered solutions are now available using integrated selection research and strategies that have been shown to outperform. These are bolstered by greater scrutiny of asset management performance and their investment processes.

The fettered approach also allows better control over asset allocation – both strategic and tactical. This is important, as it’s now generally accepted as a much more significant driver of returns, contributing over 90 per cent of returns1.

Maintaining control

Of course, adviser practices have changed significantly as well.

Advisers are increasingly interested in solutions that give them much greater control over risk and that, in turn, allow them to better deliver solutions, which remain suitable over time. They don’t want to worry about style drift or too much weighting in a particular asset.

Moreover, although the regulator does not specify what sort of investment solutions an adviser should propose to their clients, the thrust of the most recent regulatory work is about reminding advisers that they must recommend suitable plans that offer value for money and that remain on track.

Of course, this issue has been thrown into sharp relief by the recent upheavals at Woodford Investment Management, as its funds featured in many unfettered arrangements.

By contrast, a broadly fettered approach allows the overall fund manager to look through to the underlying assets. This, in turn, allows for a much higher degree of control over the portfolio than would otherwise be the case in terms of stocks and securities, sectors and currencies.

In addition, an important component of risk management is risk profiling, and ensuring that the appropriate risk profile is maintained.

Fettered funds tend to compare favourably to the controls achievable with a group of more disparate fund managers all with their own behavioural biases, some of which can arise simply because of the sector the fund is in.

In addition, although a DFM may well have reasonable communications with the managers they select (especially during the selection process), rather than receiving a daily feed, they may well only receive a monthly update providing full portfolio visibility, which puts them at a significant disadvantage.

Cost control

A fettered approach is also likely to mean much greater control of costs, partly through avoiding some altogether. There may, for example, be no switching to other funds and fund managers in a bid to catch better performance.

Tactical adjustments can be delivered much more efficiently as part of the overarching arrangement. Additionally, portfolio turnover should be lower too as it will be centrally controlled.

With one investment manager, cost-effective fees can be negotiated with the single firm and investments made in bulk. It is not a matter of approaching several investment managers with a smaller portion of money.

It also allows advisers to reduce costs in other ways, because rather than having to pay twice—once to the portfolio manager and again to the end fund manager or managers—it involves a single fee.

Of course, it is up to advisers to scrutinise and review costs on a case-by-case basis.

Last word

There is a strong case for the benefits of fettered arrangements from a cost, control and selection perspective. However, it’s worth qualifying it in one regard. The markets for almost every asset are in a state of flux, so we can envisage a situation where you might want to seek out expertise from another fund house, whilst retaining the majority with a main waterfront asset manager. You might even call that fettered but flexible.

The key for advisers is to understand the rationale and the implications for the choices taken and to ensure that it aligns with your requirements.

Read more articles via our insights page

Notes

1 The Determinants of Portfolio Performance research carried out by Brinson, Hood and Beebower and published in the Financial Analyst Journal in 1986, found that the percentage of the variability of a portfolio’s return over time that could be explained by asset allocation policy was over 90%. Ibbotson and Kaplan in 2000 found that strategic asset allocation explains around 90% of the variability of a typical fund’s returns over time, but accounts for only around 40% of the variation of returns among funds.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Fraser Blain, CCO, Horizon Funds

Fraser Blain is a sales and marketing professional with over 30 years of experience in the distribution and marketing of wholesale investment products across UK and Continental European Retail markets. Fraser’s previous experience includes National Investment Development Director at Zurich Insurance Group and Head of UK Wholesale Distribution at Allianz Global Investors UK.

Read more articles by this author

Be the first to hear news and insights from Embark Pensions

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.