With the pandemic dominating the short-term outlook, the longer-term advantages of emerging-market companies have become more important in the pursuit of return. Here are 5 positive trends:

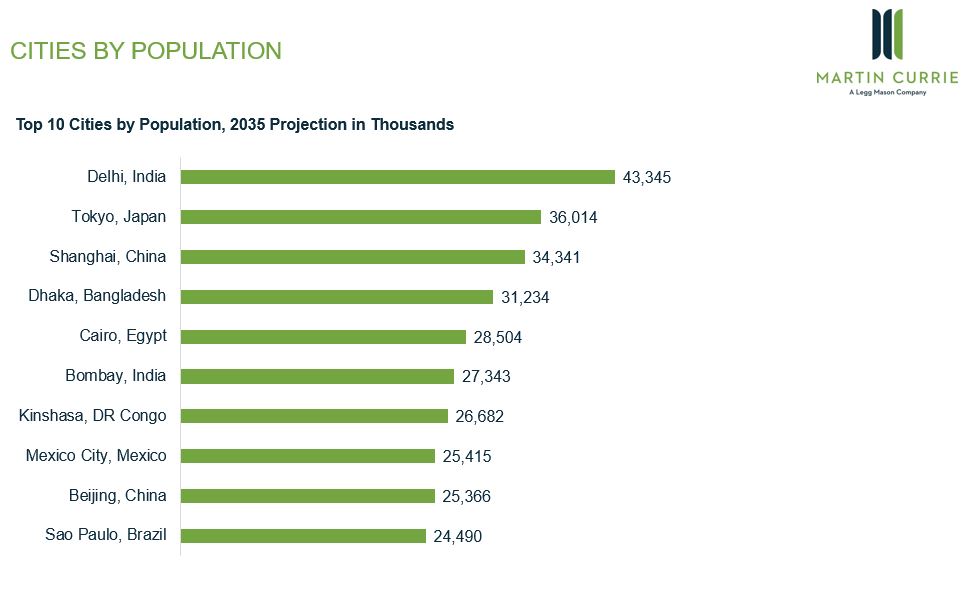

- The rise of megacities

Urbanisation remains a powerful force in emerging markets, with cities swelling in population as jobs migrate from the countryside. There are already 20 ‘mega-cities’ (i.e. with populations of over 10 million), a number that is projected to grow to 30 by 2030—largely within the Asia-Pacific region—and 9 of the 10 largest cities will be in emerging markets.1

Top 10 cities by population, 2035 projection in thousands

Source: United Nations, Department of Economic and Social Affairs. Forecasts are inherently limited and should not be relied upon as indicators of actual or future performance.

- Rising middle class

Urbanisation generally brings with it growth of the middle class in emerging markets. That’s changing consumption habits – and sparking demand for a broader range of goods and services.

The Asia Pacific region in particular is expected to see middle income growth skyrocket by 2030 with 3.5 billion people in the middle class – over 150% growth in just 15 years.2

- Embracing disruptive technologies

Emerging markets are adopting newer disruptive technologies and adapting to digital life faster than developed markets.

China is now the world’s largest e-commerce market, boasting some of the highest user rates of financial technology services for money transfer and payments, savings and investments, and borrowing. What’s more, China and South Korea are both on the front lines of future innovation – ranking among the top five countries for total patent applications.

Top five countries for patent applications

Source: Statista, World Intellectual Property Organisation. Top five ranking of national patent offices with the most patent applications in 2016.

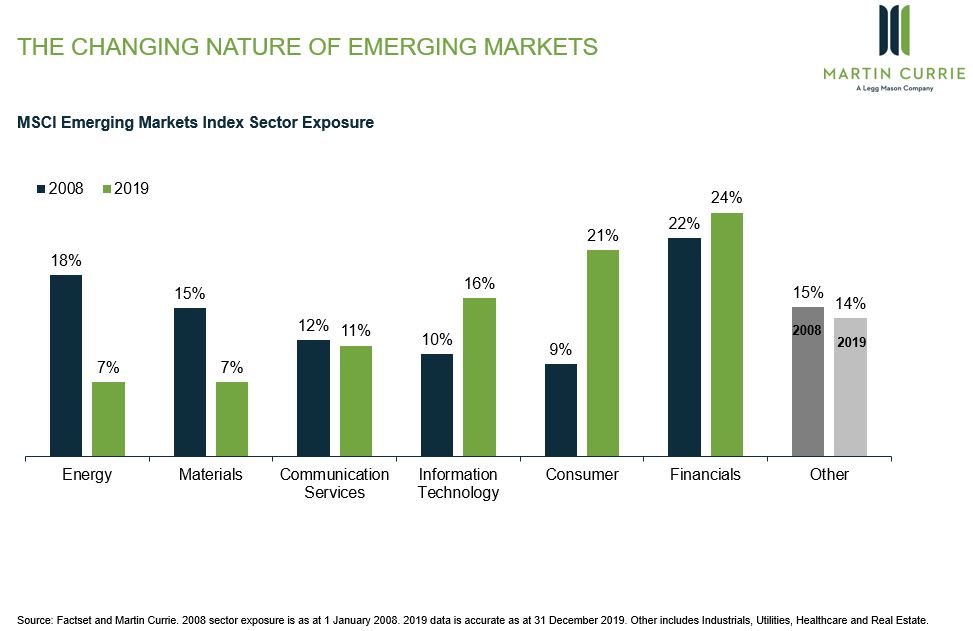

- A new business landscape

Economic diversification has changed the shape of opportunity in EM. The last decade has seen a major shift away from energy and raw materials and toward consumer, financial and high-tech. That’s allowed more EM-based companies to act as industry leaders, especially in technology.

MSCI emerging markets index sector exposure

Source: Factset and Martin Currie. 2008 sector exposure is as of 1 January 2008. 2019 data is as of 31 December 2019. Other includes Industrials, Utilities, Healthcare and Real Estate. Past performance is no guarantee of future results. Indexes are unmanaged and investors cannot invest directly in an index.

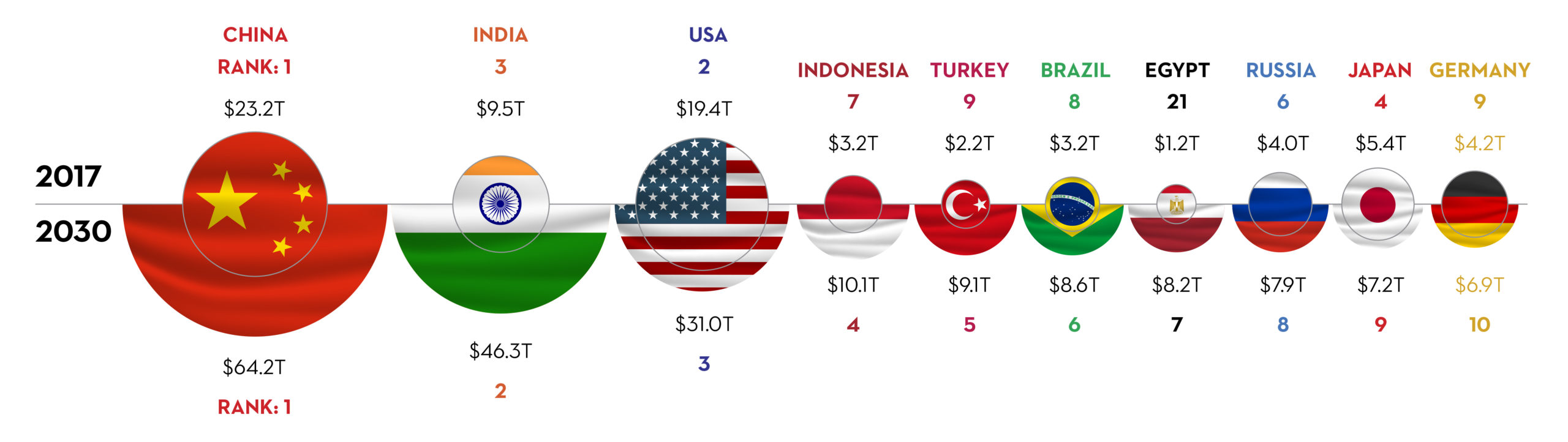

- Faster economic growth

Emerging markets are forecast to grow almost three times as fast as developed markets over the next five years. EM’s share of global GDP, already 40.2%, should rise even higher.

Seven of the world’s 10 largest economies will be “emerging” by 2030

Source: Visual Capitalist. Based on IMF (2017 data), Standard Chartered (2030 projections), Oxford Economics, Brookings Institute.

For more articles like this, please visit our insights page

Notes

1 Source: United Nations, Department of Economic and Social Affairs. Based on countries in the MSCI AC Asia Pacific ex Japan Index

2 Ibid

About the author

Martin Currie, A Legg Mason company

Martin Currie builds global, stock-driven portfolios based on fundamental research, devoting all of its resources to delivering optimum investment outcomes and superior client relationships.

Definitions

Developed markets (DM) refers to countries that have sound, well-established economies and are therefore thought to offer safer, more stable investment opportunities than developing markets.

Emerging markets (EM) are nations with social or business activity in the process of rapid growth and industrialization. These nations are sometimes also referred to as developing or less developed countries.

Environmental, Social, and Governance (ESG) refers to the three central factors in measuring the sustainability and societal impact of an investment in a company or business.

Gross Domestic Product (GDP) is an economic statistic which measures the market value of all final goods and services produced within a country in a given period of time.

The MSCI Asia Pacific ex Japan Index is a market capitalization weighted index that is designed to measure the equity market performance of the developed and emerging markets in the Asia Pacific region ex-Japan.

The MSCI Emerging Markets (EM) Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

Important Information

All investments involve risk, including possible loss of principal.

The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Legg Mason nor any of its affiliates guarantees any rate of return or the return of capital invested.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

The information in this material is confidential and proprietary and may not be used other than by the intended user. Neither Legg Mason or its affiliates or any of their officer or employee of Legg Mason accepts any liability whatsoever for any loss arising from any use of this material or its contents. This material may not be reproduced, distributed or published without prior written permission from Legg Mason. Distribution of this material may be restricted in certain jurisdictions. Any persons coming into possession of this material should seek advice for details of, and observe such restrictions (if any).

This material may have been prepared by an advisor or entity affiliated with an entity mentioned below through common control and ownership by Legg Mason, Inc. Unless otherwise noted the “$” (dollar sign) represents U.S. Dollars.

This material is only for distribution in those countries and to those recipients listed.

In the UK this financial promotion is issued by Legg Mason Investments (Europe) Limited, registered office 201 Bishopsgate, London, EC2M 3AB. Registered in England and Wales, Company No. 1732037. Authorised and regulated by the UK Financial Conduct Authority.

The information, materials or opinions contained on this website are for general information purposes only and are not intended to constitute legal or other professional advice and should not be relied on treated as a substitute for specific advice of any kind.

We make no warranties, representatives or undertakings about any of the content of this website (including without limitation any representations as to the quality, accuracy, completeness or fitness of any particular purpose of such content, or in relation to any content of articles provided by third parties and displayed on this website or any website referred to or accessed by hyperlinks through this website.

Although we make reasonable efforts to update the information on this site, we make no representation warranties or guarantees whether express or implied that the content on our site is accurate complete or up to date.

By Martin Currie, A Legg Mason company

Martin Currie builds global, stock-driven portfolios based on fundamental research, devoting all of its resources to delivering optimum investment outcomes and superior client relationships.

Read more articles by this author

Be the first to hear news and insights from Embark Pensions

Sign up to receive updates from Embark Group and its businesses. You can unsubscribe at any time using the link at the bottom of our emails, and we promise never to pass your details to a third party. Please consult our Privacy Notice for more information.